Payday Loan Statistics 2021

Data and statistics regarding the payday loan industry can be lacking insight. The industry is also constantly under fire from legislators, consumer advocate groups, and even the media at times. It’s hard to get a balanced, nuanced, fact-based reckoning of just what the payday loan industry is all about. Personal Money Network has compiled payday statistics from various lenders and sources as well as academic research. Our aim is to shed some light on the industry as a whole, as well as historical and market context for the product offered by the alternative financial services and small dollar market.

- In the United States, about 2.5 million households use at least one payday loan each year. [1]

- Legality by state of Payday Loans in the U.S. (Wikipedia) [2]

- Average payday loan borrowers earn about $30,000 per year, with about 58 percent having trouble meeting their monthly expenses. (Pew Charitable Trusts) [3]

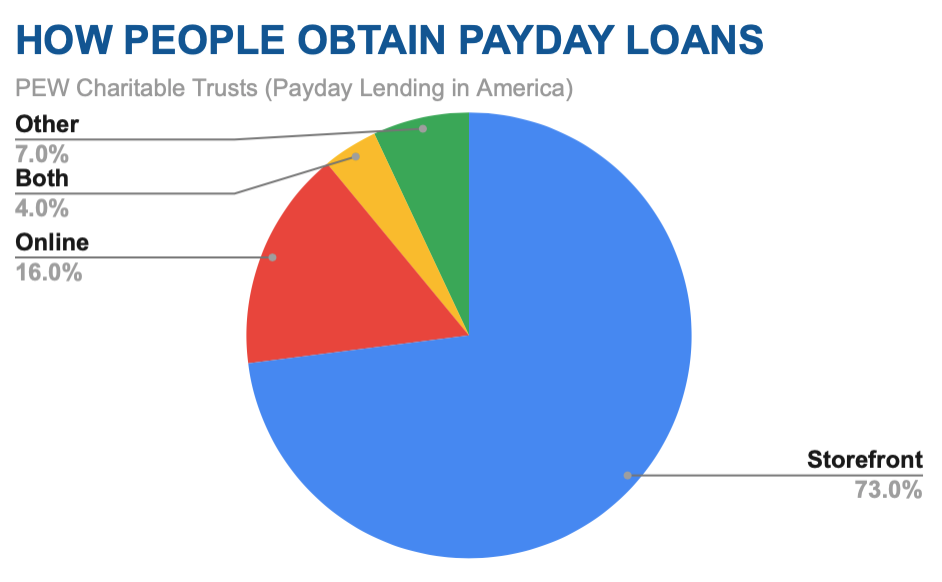

- About 70% of borrowers of payday loans are using them for their regular recurring expenses, such as rent. (Pew Charitable Trusts) [3]

- About 12 milllion Americans use payday loan products each year (Federal Reserve) [4]

- About 25% of Americans are ‘unbanked’ and and without access to traditional consumer finance options (CNBC) [5]

- About 12% of the U.S. population has a poor or bad credit score that would leave them with alternative lending such as payday loans as one of the few options available (Experian) [6]

- U.S. states with most payday lenders include New Mexico, Kentucky, Louisiana, Alabama, Mississippi, Utah, South Dakota (CreditRepair) [7]

- U.S. states with the highest interest rates and ARP (Center for Responsible Lending) [8]

Payday Lending Statistics Topics

- Demographics of borrowers

The typical payday loan borrower is not who one might think. While often portrayed as being working poor, the average payday loan borrower has an annual income of $47,620 and is likely a homeowner.

- Cost of short term credit

Payday loan fees are often described as annualized percentage rates or APR – the same standard as car loans, credit cards and mortgages that take years to pay off. Most payday loans are repaid within two weeks, but other things – such as an overdraft fee – can carry drastically higher interest rates when expressed as APR.

- Lending practices

Many are led to believe that payday loan lenders are loan sharks with a license that are preying on the poor who don’t understand the product well enough. However, the poor are not the payday lenders’ typical customers, lenders typically make terms as understandable as possible, compared to the credit card industry – where only 20 percent of customers fully understand the cost of the service.

Personal Money Network has a financial stake in the payday loan lending industry, and fully discloses that fact. However, Personal Money Network is not a direct lender, but works with many, and thus can lend a unique perspective, which will hopefully shed some light on the industry and trends within it.

While payday loans are a short term solution, they are often mentioned in terms of APR or annual percentage rate, which is incorrect. They are to be repaid by next payday.

So using the same ‘thinking’ here are some other examples you never hear of that but actually work out to be even more expensive.

Borrowing online can help you save! | |

|---|---|

| *advances are not annual; figures provided for comparison only | |

| If you have a $100 bounced check with a $34 NSF fee to be repaid in 10 days | you pay 1,241% APR |

| If you have a $100 debit card overdraft with a $37 fee paid back in 5 days | you pay 2,701% APR |

| If you have a $100 utility bill with $46 late/reconnect fees to be paid within 14 days | you pay 1,203% APR |

Sources: